Vending

Conagra Brands boosts Q3 sales and earnings

April 8, 2021

ChatGPT

ChatGPT Grok

Grok Perplexity

Perplexity Claude

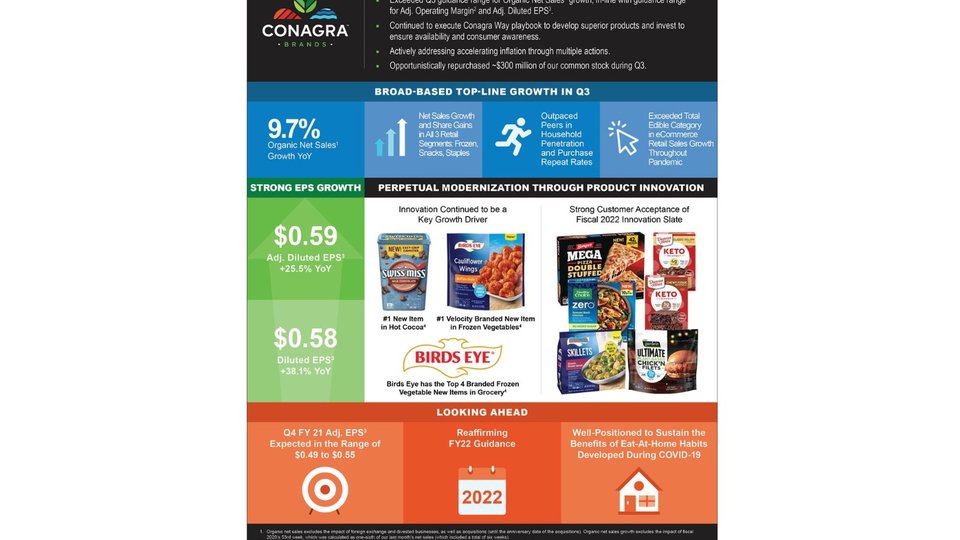

ClaudeConagra Brands Inc. net sales increased 8.5% from $2.55 billion in Q3 2020 to $2.8 billion for the third quarter ending Feb. 28, 2021, according to an earnings report.

The growth in reported net sales primarily reflected a 1.2% net decrease from the divestitures of the Lender's bagel business, the H.K. Anderson business and the Peter Pan peanut butter business, and the exit of the private label peanut butter business.

The growth also reflected a 9.7% increase in organic net sales, driven by a 6.1% increase in volume and a favorable price/mix impact of 3.6%.

The volume increase was primarily driven by continued elevated at-home food consumption as a result of the COVID-19 pandemic, which benefitted the company's retail segments. This increase was partially offset by the pandemic's negative impact on the foodservice segment as well as a temporary supply chain disruption related to a winter storm near the end of the quarter.

In the quarter, net income attributable to Conagra Brands increased 37.8% from $204.7 million in Q3 2020 to $281 million, translating in a gain from 42 cents per diluted share to 58 cents per diluted share.

Adjusted net income attributable to Conagra Brands increased 24.1% to $287 million, or 59 cents per diluted share, in the quarter. The increases were driven primarily by the increase in gross profit.

Net sales for the grocery and snacks increased 10.8% to $1.1 billion in the quarter reflecting a 2.3% decrease from the impact of the sold businesses and a 13.1% increase in organic net sales.

Volume benefited from continued elevated at-home food consumption as a result of the COVID-19 pandemic. Many snacks and staples brands experienced strong organic net sales growth in the quarter, including snack brands Orville Redenbacher's, Act II, Swiss Miss, Snack Pack and Slim Jim as well as staples brands Chef Boyardee, Libby's, PAM, Hunt's and Armour Star.

The quarterly revenue beat analyst expectations by $50 million, while the Non-GAAP earnings per share of 59 cents and GAAP EPS of 58 cents both beat expectations by one cent, according to Seeking Alpha.

Shares traded at $37.22 today against a 52-week range of $30.16-$38.98.

"We remain confident that each of our retail domains — frozen, snacks, and staples — is well-positioned to sustain the benefits of the eat-at-home habits consumers have developed during the COVID-19 pandemic," Sean Connolly, president and chief executive officer, said in the press release.

Net sales for the refrigerated and frozen segment increased 11.7% to $1.2 billion in the quarter reflecting a 0.4% decrease from the impact of the sold businesses; and a 12.1% increase in organic net sales.

Volume benefited from continued elevated at-home food consumption as a result of the COVID-19 pandemic. Marie Callender's, Birds Eye, Banquet, P.F. Chang's Home Menu and Reddi-wip were among the brands with the strongest organic sales growth in the quarter.

Net sales for the foodservice segment decreased 17.2% to $194 million in the quarter reflecting a 0.7% decrease from the impact of the sold businesses and a 16.5% decrease in organic net sales.

On an organic net sales basis, volume decreased 19.5% primarily driven by lower restaurant traffic as a result of the COVID-19 pandemic.

In the fourth quarter to-date, the company has seen a sustained increase in demand in its retail segments when compared to pre-COVID-19 demand levels, driven by continued elevated at-home eating as well as the impact of customers beginning to rebuild inventories. The company has also continued to see reduced demand in its foodservice segment when compared to pre-COVID-19 demand levels.

Based on these factors, the company is expecting organic net sales growth in the range of 10% to 12%, adjusted operating margin in the range of 14% to 15% and adjusted EPS in the range of 49 cents to 55 cents.

For an update on how the coronavirus pandemic has affected convenience services, click here.

Related Media

Subscribe

Get the latest news and resources from Vending Times.

Recent Posts